James

Fintech writer with a knack for turning complex money and crypto topics into engaging, accessible content. Whether it's demystifying blockchain or breaking down finance trends, he make sure every word counts.

Cashback pays you to buy groceries, gas, and dinner. Here's how it actually works and how to maximize it.

Imagine walking out of the grocery store and realizing you just got paid to buy your weekly groceries. Not with coupons or points that expire, but with actual cash. That’s Cashback!

For example, if you spend $200 at a grocery store with a 2% Cashback credit card, you earn $4 back. Simply put, it’s a rebate on your everyday purchases whether that’s at a supermarket, restaurant, or online shopping website.

So, let’s dive in and learn how Cashback works step by step, the different types of Cashback there are, how to calculate your rewards, and what could be the best option for you!

How Does Cashback Work?

Cashback follows a straightforward process:

- You make a purchase using your credit card.

- The merchant processes the payment through a network like Visa or American Express.

- The issuing bank calculates your reward based on the card’s rates.

- The reward accrues in your account.

Normally, you don’t receive Cashback instantly. Rewards typically appear after your monthly billing cycle closes, not at the moment of payment. If you spend $500 during a month on a 2% card, you earn $10 ($500 × 2% = $10), but you’ll see it added after your statement posts.

Cashback vs. Cash Advance

Although their names may be similar, these are not the same thing.

- Cashback is a reward.

- Cash advance is a short-term loan taken from your credit line, often with an immediate fee and a high interest rate.

Confusing the two can be costly. A cash advance may carry a fee plus instant interest, while Cashback reduces your overall expense.

Cashback vs. Points

Some cards advertise “cashback” but issue points instead. Those points may convert at a fixed rate (for example, 1 point = 1 cent), or they may have variable redemption value depending on how you use them for travel, gift cards, or online shopping. Always check the terms so you understand the true value.

Types of Cashback Cards

Not all Cashback cards work the same way. These are some of the most popular Cashback models you can find:

Flat-Rate Cards

Flat-rate cards offer the same percentage on every purchase. Typical rates range from 1.5% to 2%.

If you spend $1,000 in a month on a 2% flat-rate card, you earn $20 ($1,000 × 2% = $20), regardless of whether you spent it on retail, insurance, or streaming television.

It may be the best choice for people who prefer simplicity.

Fixed or Tiered Category Cards

These cards offer higher rates in specific categories (often grocery stores, gas stations, restaurants, or travel) and a lower rate (commonly 1%) on everything else.

Example:

- 3% at supermarkets → $500 × 3% = $15

- 1% elsewhere → $500 × 1% = $5

Total rewards = $20.

The issuing bank defines which merchants qualify, so it’s important to read the guideline and merchant terms matters.

It’s the best option for consumers with consistent spending patterns.

Rotating Category Cards

These offer 5% in categories that change quarterly, usually capped at a spending limit.

For example:

If the quarterly cap is $1,500 and you spend $1,500 at 5%, you earn $75 ($1,500 × 5% = $75). After that cap, rewards typically drop to 1%.

You must activate the bonus each quarter. Missing activation means earning only the base rate.

It’s best suited for engaged users who track deadlines and spending frequency.

Choose-Your-Own Category Cards

Some cards let you select your bonus category monthly. Others automatically apply a higher rate to your highest spending category.

If you select dining at 3% and spend $400 at restaurants, you earn $12 ($400 × 3% = $12).

It’s best for people whose lifestyle and consumption patterns change regularly.

How to Calculate Your Cashback

The formula is simple:

Amount Spent × Cashback Rate = Reward

Examples:

- $100 × 1% = $1.00

- $1,000 × 1.5% = $15.00

- $500 × 5% = $25.00

- $2,000 × 5% = $100.00

Keep in mind that spending caps and category limits can reduce your effective rate. Always review your card’s terms before assuming you’ll earn the top rate on all purchases.

Is a Cashback Credit Card Worth It?

Cashback cards work best if you pay your balance in full every month. If you carry a balance, interest charges (sometimes 20% or more annually) can easily exceed your rewards.

Pros

- You earn a percentage back on everyday life expenses.

- Rewards have fixed dollar value, unlike variable mile systems.

- Some cards have no annual fee.

- Over time, rewards can offset real costs.

For example, spending $2,000 per month at 2% earns $40 monthly ($2,000 × 2% = $40), or $480 per year.

Cons

- Carrying a balance triggers interest that outweighs rewards.

- Some cards charge annual fees.

- Rotating categories require active management.

- Applying for multiple cards can cause a temporary dip in your credit score due to hard inquiries from agencies like TransUnion.

Also consider the difference between credit and debit. A debit card pulls money directly from your bank account, avoiding interest entirely. A credit card offers rewards and credit-building potential, but it also introduces risk if spending exceeds your budget.

Cashback is an incentive, not free money. It works best when aligned with disciplined personal finance habits.

Tips to Maximise Your Cashback

- Match the card to your real spending. Review recent bank statements before choosing.

- Always pay in full. Interest eliminates profit.

- Activate rotating categories on time.

- Time large purchases strategically.

- Consider pairing cards. A flat-rate card for general purchases plus a category card for groceries or travel can increase total rewards.

- Stack with cash back apps. Services like PayPal shopping offers or cashback websites operate separately from your card rewards.

- Review welcome bonuses carefully. Many cards offer $150–$200 after meeting a spend requirement, but make sure the spending fits your normal budget.

Get Cashback Without the Credit Trap

Cash back credit cards can seem attractive: earn rewards on your spending, build credit, maybe snag some bonus points. But here's what you don’t get told upfront: if you carry a balance, even for a month or two, interest charges can wipe out any rewards you’ve earned. Suddenly that 2% cash back doesn’t look so good.

There's a better way: crypto Cashback on your debit card. Tap’s debit card gives you the rewards without the credit-related hassle. You earn cashback on everyday purchases (groceries, coffee, travel, dining) just like a credit card, but without borrowing, without interest, without the temptation to overspend, and with instant conversions. Your purchases come straight from your account balance, keeping you in control while still earning real rewards.

Tap’s Cashback isn’t paid in points or miles with obscure redemption rules. It's paid in the XTP token, deposited directly into your wallet based on the amount of XTP you have staked. Cashback rates range from 0.5% to 8%, scaling with your tier. The more XTP tokens you lock up, the more you earn. Just spend with your debit card, earn rewards automatically. If you value flexibility and financial discipline but still want to be rewarded for smart spending, then Tap’s crypto debit card is built for you!

Ready to earn Cashback the smarter way? Download the Tap app and start turning your spending into crypto rewards today!

USDS is the decentralized stablecoin built to replace DAI, backed by crypto collateral, governed by smart contracts, and designed for DeFi’s next chapter.

Built as the next evolution of DAI, USDS is a stablecoin that operates within the Sky Protocol ecosystem (formerly MakerDAO) and aims to combine price stability, transparency, and decentralization in a single digital asset.

As stablecoins play a growing role in global finance, USDS offers an alternative to centralized options by using crypto-backed collateral and automated smart contracts rather than relying on a single issuing company. Beyond price stability, USDS is designed to integrate seamlessly with decentralized finance applications, offer earning opportunities through protocol incentives, and support a multi-chain future. For users seeking a stable digital dollar without centralized control, USDS represents a modern approach to value storage and transfer.

What Is USDS?

USDS is a crypto-backed stablecoin pegged to the US dollar, meaning its target price is approximately $1 at all times. Unlike traditional digital dollars issued by centralized companies, USDS is governed by smart contracts and decentralized decision-making rather than a single authority.

The foundation of USDS rests on three core principles. First, stability: the protocol is designed to keep USDS close to its dollar peg even during market volatility. Second, decentralization: no single company or government controls issuance, freezing, or redemption. Third, collateralization: every USDS in circulation is backed by crypto assets such as ETH, USDC, and tokenized real-world assets held within the Sky Protocol.

Compared to centralized stablecoins like USDT or USDC, USDS does not depend on corporate bank reserves or off-chain custodians. Compared to DAI, USDS is built for greater scalability and multi-chain functionality. And unlike purely algorithmic stablecoins, USDS relies on tangible collateral rather than market incentives alone. Its purpose is to provide a transparent, resilient digital dollar aligned with decentralized finance values.

How USDS Works

Creation Through Sky Vaults

USDS is created through a system known as Sky Vaults. Users deposit approved collateral assets into automated smart contracts and, in return, mint USDS. A simple way to think about this is like placing valuable assets into a secure digital vault and receiving a dollar-pegged receipt that can be spent or transferred.

Accepted collateral includes cryptocurrencies such as ETH, stable assets like USDC, and certain tokenized real-world assets. Each vault operates under predefined rules that ensure system-wide consistency and security.

Stability and Overcollateralization

To protect the dollar peg, USDS is overcollateralized. This means users must deposit more value than the amount of USDS they generate. If the value of the collateral falls too far, the system automatically sells part of it through a liquidation process to protect overall stability. This safety buffer is a key reason USDS can maintain its peg without relying on a central issuer.

Role Within the Sky Protocol

USDS functions as the cornerstone stablecoin of the Sky Protocol ecosystem. It supports lending, saving, payments, and governance processes across the platform. While governance decisions are handled separately, USDS is tightly integrated into Sky’s broader architecture and incentive structure.

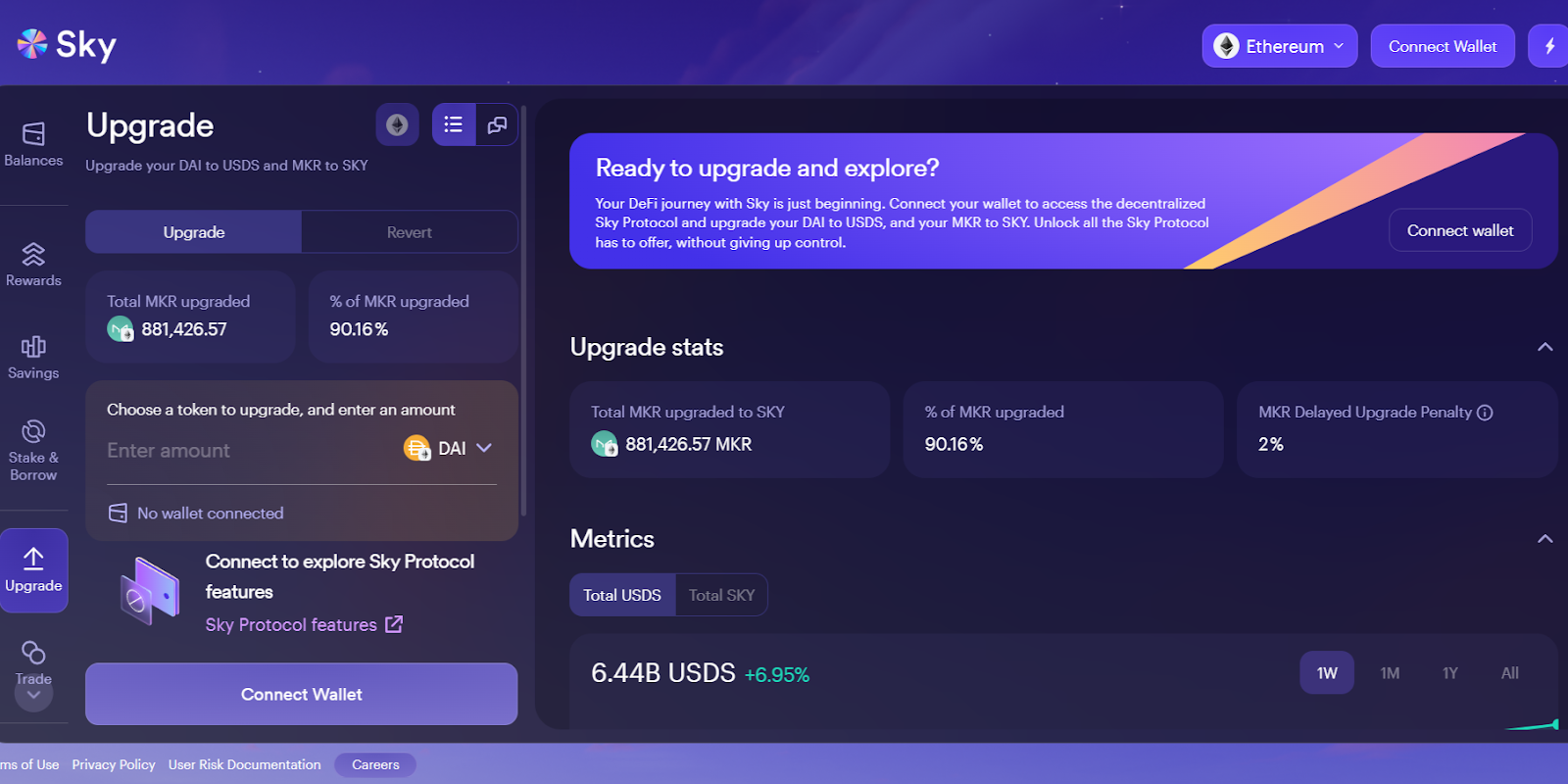

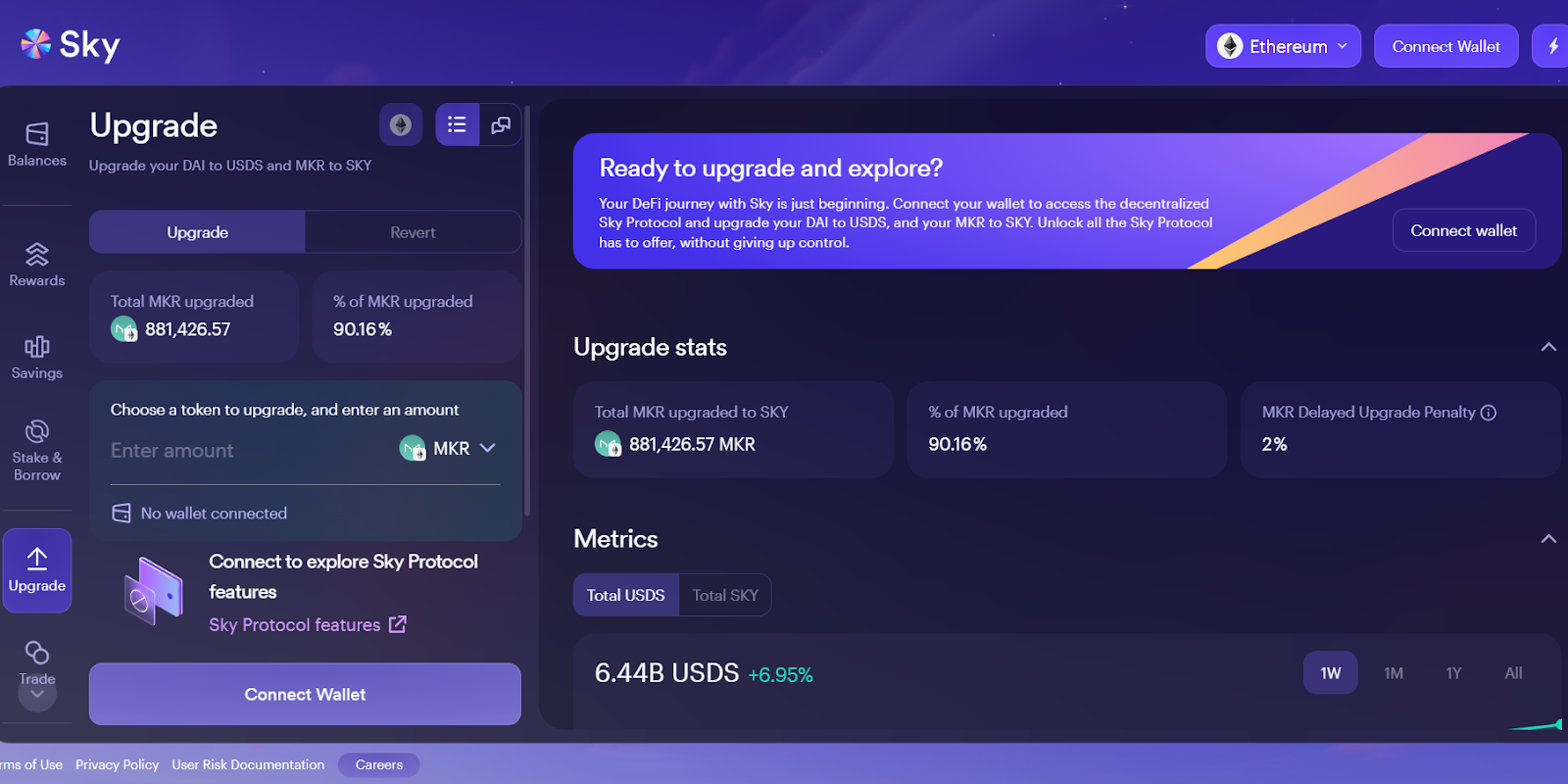

Upgrading from DAI to USDS

Transitioning from DAI to USDS is designed as a simple, user-focused service that reflects best practices in modern decentralized finance and information technology. Through the official Sky website, end users can connect a compatible cryptocurrency wallet and upgrade their DAI to y smart contract software.

From the perspective of user experience, the upgrade emphasizes accessibility, transparency, and efficiency. No centralized authority, bank, or intermediary controls the transaction, and users retain full ownership of their data and digital assets throughout the process.

Once upgraded, USDS holders can immediately access additional tools within the Sky ecosystem, including savings mechanisms and incentive programs. For users in the United States and globally, this upgrade represents not just a technical update, but an improvement in how decentralized stablecoin products deliver value, scalability, and usability.

USDS vs. DAI: What’s Changed?

USDS and DAI share a common history rooted in the MakerDAO system, now operating under the Sky Protocol. Both are decentralized stablecoins pegged to the US dollar and backed by on-chain collateral. However, USDS represents an architectural and strategic evolution focused on scalability, governance, and improved incentives for the end user.

DAI was a foundational product in decentralized finance, enabling users to lock crypto assets in smart contracts and generate a stable digital currency. USDS builds on that model by refining the underlying technology, expanding multi-chain compatibility, and introducing enhanced reward structures that improve capital efficiency and user engagement.

From a risk management and policy standpoint, USDS is designed to better align with regulatory expectations while preserving decentralization. It incorporates lessons learned from market volatility, past crises, and stablecoin design challenges, positioning USDS as a more adaptable cryptocurrency for a rapidly evolving financial ecosystem. In short, DAI laid the groundwork, while USDS applies updated design, governance, and incentive mechanisms to meet modern DeFi needs.

USDS vs. Other Stablecoins

USDS differs from other stablecoins primarily in how control, backing, and transparency are handled.

Centralized stablecoins such as USDT and USDC are issued by companies that manage fiat reserves and can freeze funds if required by policy or regulation. Algorithmic stablecoins rely mainly on market incentives and code-based supply adjustments, which can introduce higher systemic risk.

USDS, by contrast, is decentralized and collateral-backed. Its reserves are visible on-chain, and no single entity has unilateral authority over user funds. This reduces censorship risk and improves transparency, though it does make the system slightly more complex than centralized alternatives. Overall, USDS sits between institutional stablecoins and experimental algorithmic designs, offering a balance of stability and decentralization.

How to Get and Use USDS

There are several ways to acquire and use USDS, depending on user experience level.

The simplest method is purchasing USDS on a decentralized exchange using another cryptocurrency. This option is generally best for beginners. Existing DAI holders may also be able to convert DAI to USDS at a one-to-one ratio through supported platforms. More advanced users can mint USDS directly by depositing collateral into Sky Vaults.

Once acquired, USDS can be used as a stable store of value, a trading pair within DeFi markets, or a payment method for transferring value without exposure to price volatility. It also plays a role in liquidity provision and lending protocols across the decentralized finance ecosystem.

Earning With USDS

USDS offers earning opportunities through the Sky Protocol. One option is the Sky Savings Rate, which allows users to lock USDS in a smart contract and earn variable rewards over time. This approach is similar in concept to a savings account, though returns fluctuate based on protocol conditions.

Another mechanism is Sky Token Rewards, which provide additional incentives for users who actively participate in the ecosystem. These rewards are subject to change and are not guaranteed, but they offer an added layer of value for engaged users. As with all DeFi yield mechanisms, returns depend on market conditions and governance decisions.

USDS in the Sky Protocol Ecosystem

The Sky Protocol is a decentralized finance platform built on the legacy of MakerDAO. Within this ecosystem, USDS serves as the primary unit of value transfer. It interacts with governance processes, incentive programs, and other decentralized applications supported by Sky. While governance tokens and protocol upgrades play a role behind the scenes, users do not need deep technical knowledge to benefit from USDS. Its design prioritizes usability while remaining aligned with decentralized principles and transparent system architecture.

Bottom Line

USDS is a decentralized stablecoin designed to offer a reliable digital dollar without centralized control. As the successor to DAI, it builds on a proven model while introducing improved scalability and ecosystem integration through the Sky Protocol. By combining crypto-backed collateral, automated risk management, and on-chain transparency, USDS provides an alternative to both centralized and algorithmic stablecoins. As DeFi continues to evolve, USDS represents a practical option for users seeking price stability with decentralized governance.

MakerDAO just became Sky. Discover the rebranded DeFi ecosystem behind USDS stablecoin and SKY governance token, built for better accessibility and rewards.

You’ve probably heard of MakerDAO, the system behind MKR and the stablecoin DAI. Now, meet what’s next. Sky is the rebranded ecosystem behind MakerDAO, one of the most established projects in decentralized finance. Launched in 2024, Sky represents the evolution of Maker’s stablecoin and governance system, with a stronger focus on accessibility, usability, and end-user experience.

Sky builds on MakerDAO’s long-standing role in DeFi by introducing a refreshed ecosystem centered around governance and decentralized control of digital assets. So, let’s dive in and see what’s new!

What Is Sky? The MakerDAO Rebrand Explained

Sky is the new identity of MakerDAO, the decentralized finance project best known for creating DAI, now evolved into the USDS stablecoin. The rebrand reflects a broader strategic shift toward improving governance participation, streamlining business processes, and enhancing the overall user experience across the ecosystem.

The Sky ecosystem operates on the Ethereum blockchain and focuses on two core assets: USDS, a decentralized stablecoin pegged to the United States dollar, and SKY, the governance token that replaced MKR. USDS is used for savings, payments, and financial transactions, while SKY enables voting, decision-making, and long-term protocol governance.

This evolution was driven by the need for better scalability, clearer incentives, and improved accessibility for both new and existing users. By lowering governance barriers and modernizing its design, Sky aims to serve as a more intuitive decentralized application while maintaining the risk management, transparency, and stability that made MakerDAO a foundational DeFi project.

Sky vs. Skycoin: Clearing Up the Confusion

Despite the similar name, Sky (SKY) and Skycoin (SKY) are entirely different cryptocurrency projects. Sky is the rebranded MakerDAO ecosystem focused on decentralized finance, stablecoins, and governance on Ethereum. Skycoin, on the other hand, is a separate blockchain project with its own computing platform, token economics, and development team.

They differ in use case, market value, technology, and community. Sky’s primary function is enabling decentralized savings, loans, and governance through USDS and SKY, while Skycoin targets network architecture and alternative blockchain infrastructure. Their prices, market capitalization, and trading volume are also unrelated.

Understanding this distinction is important for investors and end users to avoid confusion when researching exchanges, market trends, or investment opportunities.

How Sky Works: Key Features

Sky operates as a decentralized finance service with no central authority controlling user funds. One of its core features is USDS staking, where users deposit USDS into the protocol to earn yield through mechanisms such as the Sky Savings Rate and Sky Token Rewards. This allows users to generate interest on a dollar-pegged digital currency while retaining full control of their assets.

Governance is handled through the SKY token. Token holders participate in voting on protocol upgrades, fee adjustments, collateral policies, and risk management decisions. This voting process ensures transparency and community-led decision-making across the ecosystem.

Sky also introduces a modular structure known as Sky Stars, independent projects that operate within the broader ecosystem while maintaining autonomy. This design supports innovation, scalability, and faster development, all while preserving alignment with Sky’s core financial services.

How to Upgrade from MKR to SKY

As part of the MakerDAO rebrand, MKR has been replaced by SKY as the sole governance token of the Sky Protocol. While MKR may continue to trade on secondary markets, only SKY grants access to governance, staking, and participation in the Sky ecosystem.

The upgrade process is handled directly through Sky’s official website, ensuring a non-custodial and user-controlled experience. Users simply connect their Ethereum wallet, initiate the upgrade, and convert MKR to SKY at the fixed ratio of 1 MKR = 24,000 SKY. Throughout the process, users retain full control of their assets.

Upgrading is strongly encouraged for anyone who wants to continue voting, delegating, or interacting with Sky’s governance and reward mechanisms. Holding SKY unlocks features such as protocol voting, participation in decision-making, and access to staking-related functionality tied to the Sky ecosystem.

It’s also important to note that the protocol introduces a time-based penalty for delayed upgrades. Starting September 18, 2025, the amount of SKY received per MKR will gradually decrease, beginning with a 1% reduction and increasing over time. Upgrading before this date ensures users receive the full conversion value with no penalty.

In short, while MKR remains a recognizable asset, SKY is the token that will power the Sky ecosystem going forward, and upgrading is the recommended path for anyone looking to stay aligned with the protocol’s future development.

Sky Token (SKY) Current Value & Market Performance

The SKY token plays a central role in governance and protocol incentives. Following the rebranding, MKR was converted into SKY at a 1:24,000 ratio, significantly lowering the unit price and improving accessibility for individual participants.

At the time of writing, its market capitalization places it in the top 50 cryptocurrencies, among well-established DeFi governance tokens. However, like all cryptocurrencies, SKY experiences price volatility influenced by broader market conditions and DeFi adoption trends.

Bottom Line

Sky is the next chapter of MakerDAO, reimagined to deliver a more accessible and scalable decentralized finance ecosystem. By combining USDS for savings and transactions with SKY for governance and decision-making, Sky aims to empower users with greater control, transparency, and financial autonomy.

Owning cryptocurrency is one thing. Using it in everyday life is another. While digital assets like Bitcoin and Ethereum have grown in popularity as investments and payment alternatives, spending them directly at a coffee shop, grocery store, or restaurant is not always straightforward. The vast majority of businesses still only accept fiat money, not crypto.

Crypto cards exist to solve this problem. They act as a bridge between blockchain-based assets and traditional payment systems, which allows you to spend cryptocurrency through familiar card networks like Visa and MasterCard. So, get ready! We’ll show you what crypto cards are, how they work behind the scenes, how crypto debit and credit cards differ, and even how your business can take advantage of them!

What Is a Crypto Card?

A crypto card is a payment card that lets you spend cryptocurrency in everyday transactions, even though merchants receive fiat currency such as the United States dollar or euro. From the end user’s perspective, the experience closely resembles using a traditional debit card or credit card.

Crypto cards are typically issued by a cryptocurrency exchange, fintech company, or financial services provider in partnership with an issuing bank and a payment processor. Most operate on established card networks like Visa or MasterCard, which gives them broad acceptance across retail, e-commerce, and travel services.

These cards are connected to a cryptocurrency wallet or account balance. When you make a purchase, your digital assets are automatically converted into fiat money at the current exchange rate. Crypto cards can be physical or virtual, used via a mobile app or digital wallet, and often include features such as transaction tracking, balance visibility, and loyalty incentives.

How Crypto Cards Work: The Mechanics

Although crypto cards feel familiar at checkout, several processes happen in the background to make each financial transaction possible.

Step 1: Loading Cryptocurrency

Before you can spend, you need to fund your card. This usually involves transferring cryptocurrency from an external wallet, a cryptocurrency exchange like Binance or Gemini, or an internal platform wallet. Some providers allow direct wallet linking, while others require you to move assets into a custodial account first.

Depending on the service provider, you may need to convert your crypto into a supported asset or stablecoin before spending. This step ensures compatibility with the card’s computing platform and settlement process.

Step 2: Making a Purchase

You use a crypto card just like any debit or credit card. It works online, in retail stores, at automated teller machines, and anywhere card payments are accepted. The merchant does not need to support blockchain technology or digital assets.

From the merchant’s point of view, this is a standard card payment. They never interact with cryptocurrency directly, which improves accessibility and reduces friction across the payment ecosystem.

Step 3: Automatic Crypto-to-Fiat Conversion

This is the core innovation. When you make a purchase, the card provider converts your cryptocurrency into fiat money in real time or near real time. The conversion uses the current market price, adjusted for spreads or fees.

Your crypto balance is reduced by the equivalent amount, while the merchant receives fiat currency through the traditional payment network. Exchange rates, volatility, and conversion fees can all influence the final cost.

Step 4: Transaction Settlement

The transaction is processed through established banking infrastructure and settled in one to three business days. You can view the transaction details in your mobile app, including price, currency used, fees, and timestamps.

This hybrid structure combines blockchain-based assets with legacy banking systems, allowing crypto to function within existing financial markets.

Crypto Debit Cards vs. Crypto Credit Cards

Crypto cards generally fall into two categories, each serving different preferences and risk profiles.

Crypto Debit Cards

Crypto debit cards operate on a prepaid model. You can only spend what you already hold in your account or wallet.

Pros

- No borrowing or debt

- Easier approval with minimal credit requirements

- Strong spending control

- Often suitable for stablecoin users

Cons

- Limited to available balance

- Conversion fees may apply

- Fewer premium rewards

It’s best for: Newbie users, budget-conscious consumers, and those avoiding credit risk.

Crypto Credit Cards

Crypto credit cards allow you to borrow up to a line of credit and repay later. Some use traditional credit underwriting, while others are backed by crypto collateral.

Pros

- Rewards paid in cryptocurrency

- Grace periods for repayment

- Preserves crypto holdings longer

- May help build or maintain credit score

Cons

- Interest charges if balances aren’t paid

- Annual fees common

- Higher complexity and risk

It’s best for: Experienced users seeking rewards, flexibility, and stronger purchasing power.

Key Benefits of Crypto Cards

One of the most compelling benefits of crypto cards is that they let you spend your digital assets in everyday life without worrying about merchant acceptance. Whether you’re buying groceries, paying for travel, or subscribing to online services, the payment experience mirrors traditional cards. It’s seamless and familiar.

Beyond accessibility, crypto cards offer genuine convenience and speed. Transactions happen quickly, without the need for manual selling or bank transfers. Everything from spending to tracking happens in one interface, improving both usability and financial control. This streamlined experience eliminates the friction that typically comes with converting crypto to fiat.

Many providers also offer loyalty programs that reward spending with cryptocurrency instead of points. Over time, this can actually increase your digital asset portfolio through routine consumption. Also, because crypto cards run on established networks like Visa and Mastercard, they’re widely accepted across borders. This makes them especially useful for travel, foreign exchange convenience, and international purchasing. You get the global reach of traditional payment systems combined with the flexibility of digital assets.

Security and control are also built into most crypto card platforms. Features like two-factor authentication, transaction alerts, card freezing, and detailed spending analytics support both trust and data integrity, giving you peace of mind while you spend.

Important Considerations Before Using a Crypto Card

Before jumping in, it’s worth understanding the costs involved. Crypto cards can include transaction fees, conversion spreads, ATM fees, and foreign exchange markups. Comparing fees across providers is essential to avoid surprises.

Taxes are another critical consideration. In many jurisdictions, including the United States, converting crypto to fiat is a taxable event. This means each transaction may trigger capital gains reporting, requiring careful record keeping throughout the year. If you’re a frequent spender, this is something to keep in mind.

Volatility risk is also something to keep in mind. Cryptocurrency prices fluctuate constantly, and the value of your assets may change between the time a transaction is authorized and when it settles. Using stablecoins can help reduce this risk, offering more predictable purchasing power without the wild swings.

Finally, not all crypto cards are available in every country. Regulatory environments, banking partnerships, and compliance rules vary significantly by geography, so it's important to confirm that your chosen provider operates in your region before signing up.

How to Get a Crypto Card

Step 1: Choose a Provider

Evaluate supported cryptocurrencies, card type, fees, rewards, geographic availability, and reputation. Avoid choosing based on advertising alone.

Step 2: Create an Account and Complete KYC

Most providers require identity verification under Know Your Customer regulations. This may include uploading an ID and confirming personal information.

Step 3: Fund Your Account

Deposit cryptocurrency from a wallet or exchange. Some platforms allow direct purchases using a bank account or debit card.

Step 4: Order Your Card

You may receive a virtual card instantly, with a physical card shipped later. Card issuance fees may apply.

Step 5: Activate and Set Preferences

Activate the card, configure spending limits, enable security features, and begin using it for purchases.

Where Can You Use Crypto Cards?

Crypto cards work anywhere Visa or MasterCard is accepted. This includes online retailers, physical stores, restaurants, grocery stores, and many ATMs. Some restrictions may apply for certain merchant categories or cash-equivalent transactions.

Launch Your Own Branded Crypto Card with Tap

If you want to take your business to the next level, offering a branded crypto card can transform your users’ experience. Tap’s Cards-as-a-Service program enables you to launch a fully customized crypto card program without building banking infrastructure from scratch. You can issue both physical and virtual cards suited to your needs.

Traditional card issuing can take years and require substantial investment. Tap shortens this timeline, enabling you to launch a branded crypto card program in as little as 12 weeks. Cards are fully customizable to reflect your brand identity, and the platform scales effortlessly whether you’re issuing hundreds or millions of cards.

Ready to bridge the gap between crypto and everyday spending? Get in touch with Tap's team today and discover what a tailored crypto card program can do for your business.

In 2025, millions of people stopped waiting for the financial system to provide faster and cheaper alternatives for payments. They simply started using something else. Millions of users across 15 countries have gradually started receiving slices of their income in stablecoins, and they aren’t looking back.

Stablecoins: An Everyday Currency

A new survey conducted by YouGov across 4,658 crypto users and prospective holders, puts some hard numbers to what was previously more anecdote than data. The results paint a picture of stablecoins that looks very different from the speculative, volatile image that crypto has long carried: 39% of respondents said they already receive income in stablecoins, accounting for roughly 35% of their annual earnings on average. These aren’t side hustles necessarily. For many, this is primary income.

The spending side is catching up too. More than a quarter of stablecoin holders, 27%, use them for routine purchases, carrying an average of around $200 in their digital wallets for day-to-day transactions. More than half said they had deliberately chosen a merchant specifically because they accepted stablecoins. In emerging markets, that number jumps to 60%.

The geography of adoption is telling. Ownership is higher in lower- and middle-income economies; 60% of respondents in those regions hold stablecoins versus 45% in wealthier countries. Africa stands out sharply, posting the highest ownership rate globally at 79% and the steepest year-over-year growth. The pattern makes sense: where banks are slow, remittances are expensive, and currencies are unstable, a dollar-pegged digital asset that travels instantly and cheaply is less of a novelty and more of a lifeline. Users making cross-border transfers reported saving approximately 40% on fees compared to traditional remittance services, a number that hits differently when you're sending money home every month.

The reasons people give for using stablecoins aren’t ideological. Lower transaction costs, better security, and global accessibility top the list. This isn’t a movement of crypto idealists, it’s a pragmatic shift by people who found a tool that works better for their specific situation.

Demand for deeper integration with the existing financial system is also clear. 77% of respondents said they would open a stablecoin wallet if their primary bank or fintech provider offered one, and 71% said they’d want a debit card linked to their stablecoin balance. The infrastructure gap between crypto and conventional banking, it seems, is one most users would happily see closed.

Stable Expansion

The timing matters too. The passage of the GENIUS Act in the U.S. and the rollout of Europe’s MiCA regulation have added regulatory scaffolding that’s accelerating corporate moves into the space. Payroll platform Deel announced recently that it will offer stablecoin payments, starting with U.K. and EU workers, before expanding to the U.S.

The shift can be seen on-chain, with a dramatic increase in the volume of stablecoin transactions in recent years, often running into the trillions. The total stablecoin market now sits around $307 billion, up from $260 billion around the time the GENIUS Act was signed. The trajectory is hard to argue with, and it’s not showing signs of stopping. The growth is real, and increasingly, so are the paychecks.

Bottom Line

What began as a niche tool for crypto traders has become a financial backbone for millions of people worldwide: one that’s faster, cheaper, and more accessible than the systems it’s starting to replace. And with regulatory clarity arriving on both sides of the Atlantic, businesses and institutions are no longer sitting on the sidelines. Banks, fintechs, and payroll platforms are moving in, and users are ready to meet them there. For them, stablecoins aren’t an experiment anymore. They’re just how money works now.

Launching a card program is easier than ever. Today, thanks to modern technology, businesses can issue digital debit, credit cards or virtual cards faster than ever. The real challenge comes next: how do you turn a card program into a sustainable source of revenue?

Many card programs start with a strong focus on customer acquisition and distribution. Cards are issued, users sign up, and transactions begin to flow. But without a clear monetization strategy, growth alone rarely leads to profitability. Margins are thin, regulation limits certain fees, and relying on a single revenue stream is rarely enough.

Successful card programs approach monetization as a business model decision, not an afterthought. They understand how money moves through the payment ecosystem, which revenue streams are available to them, and how card usage behavior directly impacts results. So, dive in and learn how card programs generate revenue, why active usage matters more than total cards issued, and which monetization levers matter most in practice.

The Foundation: How Card Programs Generate Value

Before discussing monetization, it’s essential to understand how a card transaction actually works and where value is created. A typical card payment follows a familiar flow: the cardholder makes a purchase with a merchant using funds from their bank account, the merchant’s acquiring bank processes the transaction, the card network (such as Visa or Mastercard) routes it, and the issuing bank ultimately approves and settles the payment. Behind the scenes, multiple parties exchange data, manage financial risk, and move money.

From a revenue perspective, several fees are involved. Merchants pay a merchant service charge, which is split across the ecosystem. A portion goes to the card network as assessment fees, another to processors, and a key portion goes to the issuer as interchange revenue. Depending on your role in the value chain, your business may earn revenue directly as the issuer or indirectly through revenue sharing with an issuing bank or program manager. Ultimately, your program structure determines which monetization options are available and how scalable they are.

Why Active Cardholders Drive Monetization

One of the most common mistakes in card programs is focusing on the total number of cards issued rather than how often those cards are actually used. There is a critical difference between issued cards, activated cards, and active cardholders. An issued card that sits unused generates no interchange, no FX revenue, and no long-term value. In contrast, a smaller base of highly active users can outperform a much larger but disengaged audience.

Active usage directly impacts every meaningful metric: transaction volume, revenue per user, retention, and customer lifetime value. This is why successful programs aim to become a user’s top-of-wallet choice, not just a backup payment method. Features like real-time notifications, budgeting tools, mobile app usability, loyalty incentives, and seamless acceptance all contribute to habitual usage.

For example, 500 cardholders making frequent purchases often generate more gross income than 2,000 cardholders who only transact once a month. Monetization scales with engagement, not vanity metrics. Any sustainable revenue model must therefore start with a clear plan for activation, retention, and ongoing card usage.

Five Core Revenue Streams for Card Programs

Most profitable card programs rely on multiple layered revenue streams rather than a single source. Below are the five most important ones.

1. Interchange Fees: The Core Revenue Stream

Interchange is the fee paid by the acquiring bank to the issuing bank for each card transaction. It is typically calculated as a percentage of the transaction value, sometimes combined with a fixed fee. Interchange rates vary based on card type, region, merchant category, and whether the payment is card-present or online.

Regulation plays a major role. In the United States, for instance, debit interchange is capped for large banks under the Durbin Amendment, while credit card interchange remains largely uncapped. In Europe, interchange caps are stricter across both debit and credit cards. Commercial and business cards often command higher interchange but require different distribution strategies.

While interchange is foundational, it is rarely sufficient on its own. Operating costs, fraud management, compliance, and customer support quickly erode margins. Modern card programs treat interchange as a baseline, not the entire business case.

2. Subscription and Membership Fees

Many programs introduce monthly or annual fees tied to premium features. These may include higher spending limits, enhanced customer service, insurance benefits, advanced expense management, or exclusive rewards.

Subscription revenue offers predictability and improves cash flow, but it only works when the value proposition is clear and the pricing game is played smartly. Consumers and businesses are increasingly sensitive to pricing, and poorly justified fees can increase churn. Tiered pricing models are often more effective, allowing users to choose a plan aligned with their needs.

3. Foreign Exchange (FX) Revenue

FX revenue is generated when cardholders spend in a foreign currency. Issuers may apply a markup to the network exchange rate or share in FX margins with partners. This model is particularly relevant for travel, cross-border commerce, and international users.

However, competition has intensified. Transparency requirements and “zero FX fee” positioning have reduced margins. FX revenue tends to be meaningful only at scale or when international usage is central to the product experience.

4. Interest and Financing (Credit Programs Only)

For credit card programs, interest income from revolving balances and installment plans can be a significant revenue stream. Annual percentage rates (APR), deferred payments, and buy-now-pay-later structures fall into this category.

This model requires robust risk management, regulatory compliance, and access to capital. It is not applicable to debit or prepaid programs but can dramatically change unit economics when executed responsibly.

5. Card Network Incentives

Visa, MasterCard, and American Express offer incentive programs to encourage issuance, usage, and international acceptance. These incentives may be volume-based, activity-based, or tied to specific launch milestones.

While often overlooked, network incentives can meaningfully offset early costs for growing programs. Negotiation, reporting accuracy, and long-term partnership strategy all influence how much value a program captures here.

The Three Pillars of a Monetizable Card Program

Revenue streams only work when supported by a strong product strategy. In practice, successful programs are built on three pillars.

First, they solve a real problem. This may involve simplifying payments, improving expense control, increasing acceptance, or offering better visibility into spending. Cards that exist without a clear use case struggle to drive consistent transactions.

Second, they deliver perceived value, not just functional utility. Trust, brand, personalization, and incentives all influence whether a user chooses one card over another. Emotional factors often determine top-of-wallet status.

Third, they target the right audience from day one. Consumer cards, business cards, travel cards, and industry-specific programs all monetize differently. Product-market fit determines which revenue streams are viable and how quickly they scale.

By understanding card economics, prioritizing active usage, and layering multiple revenue streams, businesses can build card programs that generate real, sustainable value. From here, the next step is execution: choosing the right partners to turn strategy into results.

Unlock Your Potential with Tap's White-Label Card

Tap’s white label card program supports both physical and virtual cards, giving you flexibility to align your monetization strategy with your business model and user base. Because Tap handles the heavy lifting, you can focus on what drives profitability: activation, engagement, and turning issued cards into active cardholders. The metric that matters the most.

Traditional card issuing can take years and drain resources before you see a return. Tap enables you to launch a fully functional custom card in as little as 12 weeks.

Ready to turn payments into profit? Get in touch with Tap's team today.

Three cards. Three paths. One goal. Today, if you need to handle payments, you have more options than ever before. Debit cards, credit cards, and prepaid cards are all widely used for everyday spending, online shopping, travel, payroll, and digital payments. While they can look similar and may carry logos from Mastercard or Visa, the way each card handles money, fees, risk, and consumer protection is fundamentally different.

Understanding these differences matters for budgeting, personal finance, decision-making, and security. Whether you are a consumer managing everyday life or a business evaluating card products for customers, knowing how each card type works helps ensure the right fit for specific needs, regulations, and usage scenarios.

So, jump in! Let’s break down how debit, credit, and prepaid cards work, and how they compare!

Quick Comparison Overview

Simply put, the main difference comes down to where the money comes from and when payment happens.

- Debit card: Uses money directly from a linked bank account or deposit account. Payments are deducted immediately.

- Credit card: Uses borrowed money provided by an issuing bank. Payments are settled later, often with interest if not repaid in full.

- Prepaid card: Uses money loaded in advance. Not typically linked to a bank account and cannot exceed the preloaded balance.

Debit and prepaid cards help control spending by limiting access to available funds. Credit cards introduce deferral, interest, and credit risk but offer stronger consumer protection and rewards. These differences affect fees, acceptance, regulation, and suitability for different consumers and businesses.

What Is a Debit Card and How Does It Work?

A debit card is directly linked to a bank account or credit union account. When a consumer makes a financial transaction, the funds are withdrawn from their deposit account almost instantly and reflected on their bank statement.

Debit cards are commonly used for everyday purchases, ATM withdrawals via an automated teller machine, bill payments, and point-of-sale transactions. Some retailers allow cash back at checkout, making debit cards a practical alternative to cash.

Key characteristics of debit cards include:

- Access to money you already have on deposit

- No interest or annual percentage rate

- Wide acceptance in retail, e-commerce, and mobile app environments

- Optional overdraft features, often with a fee

From a limitation perspective, debit cards do not help build a credit score and may offer less protection than credit cards in cases of theft or fraud. Since transactions impact the bank account immediately, compromised personal data can affect liquidity until disputes are resolved.

What Is a Credit Card and How Does It Work?

A credit card allows consumers to borrow money from an issuing bank up to an approved credit limit. Each purchase creates a loan that must be repaid according to the card’s terms. If the balance is not paid in full by the due date, interest is charged based on the card’s annual percentage rate.

Credit cards operate on a billing cycle rather than instant settlement. This deferral makes them useful for large purchases, travel, online shopping, and expense management.

Core features of credit cards include:

- Credit checks and approval requirements

- Monthly statements and repayment schedules

- Interest charges, fees, and fine print

- Strong consumer protection and dispute rights

Credit cards can build credit history and support loyalty programs, cashback websites, and incentives. However, they also introduce credit risk, potential debt accumulation, and higher costs if balances are carried long term.

What Is a Prepaid Card and How Does It Work?

A prepaid card is funded with money loaded in advance and is not usually linked to a traditional bank account. Once the balance reaches zero, the card cannot be used unless additional funds are deposited. This structure makes prepaid cards a controlled payment tool rather than a credit product.

Funds can typically be loaded through direct deposit (such as payroll or tax refunds), bank transfers, cash loads at retailers, or digital wallets like PayPal. Many prepaid cards are issued on major networks, enabling broad acceptance for purchasing and e-commerce payment systems.

Common prepaid card types include:

- Reloadable prepaid cards

- Gift cards and promotional merchandise cards

- Payroll cards

- Government benefit cards

Addressing common questions: prepaid cards can usually be used at ATMs, though fees vary by provider. Funds do not expire if the card is replaced. Visa and MasterCard branded prepaid cards often support chargebacks, though protections may be more limited than credit cards. Acceptance issues can occur with hotels, car rentals, or merchants requiring advance payment holds.

Prepaid cards are popular for budgeting, gifting, controlled spending for students or dependents, and use cases where a bank account or credit check is not desirable.

Debit Card vs. Credit Card: Key Differences

The primary distinction between debit and credit cards is ownership of funds. Debit cards use the consumer’s own money, while credit cards use borrowed capital.

Debit card payments are immediate and tied to account balances. Credit card payments are deferred and settled later. Debit cards avoid interest but do not build credit. Credit cards can improve a credit score but introduce interest, fees, and liability if mismanaged.

Debit cards are often preferred for daily spending, budgeting, and ATM access. Credit cards are better suited for travel, higher-value purchases, online shopping, and situations requiring stronger consumer protection.

Prepaid Card vs. Debit Card: Key Differences

Prepaid cards and debit cards are often confused because both limit spending to available funds. The critical difference is the bank account requirement.

Debit cards require a bank or credit union account and provide direct access to deposits. Prepaid cards operate independently and require funds to be loaded first. Prepaid cards typically do not allow overdrafts, making them more restrictive but easier to control.

Prepaid cards are frequently used for gifting, payroll distribution, and controlled spending. Debit cards are better suited for general-purpose banking and long-term financial management.

Prepaid Card vs. Credit Card: Key Differences

Prepaid cards and credit cards sit at opposite ends of the payment spectrum. Prepaid cards use preloaded money and do not require repayment. Credit cards use borrowed money and require monthly payments.

Prepaid cards do not impact credit scores and usually avoid interest. Credit cards require approval, involve interest, and contribute to credit history. Each serves a distinct role depending on the consumer’s financial situation, risk tolerance, and spending behavior.

Launch Your Debit Card Program with Tap

If you are considering launching a custom card for your business, Tap's white label card program lets you issue fully branded cards that connect directly to user accounts, strengthening engagement and creating new revenue possibilities. Tap handles the heavy lifting, allowing you to launch a fully functional program in as little as 12 weeks instead of years.

Ready to explore what a white-label debit card could do for your business? Get in touch with Tap's team today.

You don’t need to call your bank to issue a debit card anymore. That world is gone. Today, all sorts of brands can launch branded debit card programs by partnering with all sorts of financial licensed institutions. It doesn’t matter if you’re managing gig-economy payouts, or operating any business where users hold balances. Your business can be anything! A debit card program can increase engagement, strengthen loyalty, unlock revenue through fees, and give users seamless access to their funds.

We’ll show you what a debit card program actually is, why businesses launch them, how they differ from credit cards and prepaid cards, what they cost, and the exact steps required to bring one to market. But first a little spoiler: despite the tools that modern technology puts at our disposal, launching a program from scratch isn’t for everyone.

What Is a Debit Card Program?

A debit card program will allow your business to issue a branded card that dares funds directly from a linked bank account. So, when a user makes a purchase, money is deducted immediately from their balance. This is the main difference with credit cards, which extend credit and fall under an entirely separate set of rules and regulations. Debit cards work under electronic funds transfer regulations and require real-time computing to check balances and prevent overdrafts. Simple enough, right?

Here’s what’s important to understand. Launching a debit card program does not mean starting a bank. Creating a bank requires tens of millions in capital, years of regulatory approval, and expertise in risk, compliance, and a whole ecosystem of banking operations. A debit card program, by contrast, is built through partnerships with licensed banks that act as issuers and BIN sponsors. Programs can support physical debit cards, virtual cards for online payments, or both. They are commonly used for consumer banking apps, employee spending, payroll access, gig-economy payouts, etc.

Why Launch a Debit Card Program?

If your business already manages user balances or financial workflows, debit cards unlock real advantages. First, debit cards increase customer engagement. First, debit cards increase customer engagement. Every transaction becomes a brand touchpoint. This means there will be constant interaction with your mobile app or platform. Second, they strengthen customer loyalty by keeping spending within your ecosystem rather than external wallets or banks. If your users can access their money through your card, they are less likely to move their funds elsewhere.

Debit card programs also provide data insights into spending behavior. This means you will learn more about their transaction frequency, and usage patterns, and this in turn will lead to better product decisions and personalization. You will also see what merchants your users prefer and when they spend. This information is invaluable for improving your users’ experience.

From a revenue perspective, businesses earn interchange fees on each transaction, creating usage-based income. Every swipe, tap, or online payment generates a small fee, and at scale, those fees can add up to a meaningful revenue stream. Debit cards will also simplify operations by giving you access to funds for customers, employees, or contractors. This will reduce issues regarding payments, withdrawals, and everyday spending.

Common use cases are neobanks issuing consumer debit cards, payroll platforms offering instant wage access through direct deposit cards, or marketplaces enabling wallet-to-card functionality so freelancers and gig workers can access earnings immediately.

Debit Card vs Other Card Types: Understanding the Difference

Debit cards can be confused with other card products, but the differences matter. Let’s go through a quick comparison to set the record straight.

- Debit cards are linked to a bank account and only allow spending of available funds. Users do not undergo credit checks, and transactions settle in near real time using real-time computing infrastructure. Because there's no credit risk, the regulatory framework is simpler.

- Credit cards extend a line of credit, require underwriting to assess risk, and are governed by lending regulations such as the Truth in Lending Act in the U.S., for instance. They carry higher interchange fees and greater risk for the issuer.

- Prepaid cards hold a stored balance that is loaded in advance and is not necessarily tied to a traditional bank account. They follow different compliance rules and are commonly used for gift card programs, incentive rewards, subscription services, or travel. Prepaid cards can be useful, but they lack the direct connection to a user’s finances.

How Much Does It Cost to Launch a Debit Card Program?

Costs vary based on scale, features, and geography, but you can expect them to follow a similar pattern. Let's break it down. You can expect smart cards to cost you between $2 to $10 dollars per card. The production of cards accounts for plastic and chips with integrated circuits. You can expect cards with near-field communication (NFC) to cost more, while premium cards such as metal cards can cost as much as $20 dollars simply to produce.

Beyond the cost of acquiring the cards you need, you will need to spend on BIN sponsorship applications, legal review, and card design. Then you will need to pay for ongoing expenses like technology fees, BIN sponsorship, compliance monitoring, fraud detection systems, and customer support infrastructure. In short, you can easily expect costs to surpass $100,000 in the first year of your program.

Key Requirements for Launching a Debit Card Program

- Bank partnership to sponsor the program.

- Registered business entity to be in a good legal and financial standing.

- Compliance infrastructure such as KYC, AML, and fraud monitoring.

- Technology stack for card management APIs and account systems.

- Operating capital to support settlements and growth.

- Customer support to dispute handling and cardholder assistance.

- Security standards such as PCI DSS and data protection controls.

To launch a debit card you will need to sort out these factors first. Partnering up with a bank will take care of most of these, but you’re still responsible for understanding how they work and ensuring your program meets regulatory standards.

Step-by-Step Guide to Launching Your Debit Card Program

Step 1: Define Your Debit Card Program Objectives

Start by identifying who the card is for: customers, employees, contractors, or students. Clarify use cases such as daily spending, ATM withdrawals, online payments, or payroll access. Are you trying to improve user experience, create a new revenue stream, or reduce friction in your existing workflows?

Decide whether you’ll issue virtual cards, physical cards, or both. Virtual cards can be issued instantly and are great for online commerce, streaming media subscriptions, and digital purchases. Physical cards take longer to produce and mail but are essential for point of sale transactions and ATM access. Estimate expected card volume and budget. How many users do you expect in year one? What's your target market? What's your projected transaction frequency? These numbers will guide your partnership conversations and help you understand the full cost and resource requirements.

Step 2: Choose Your Debit Card Program Model

Select the structure that fits your business. Open-loop debit cards work anywhere Visa or Mastercard is accepted, giving users maximum flexibility. White-label programs keep your brand front and center, while co-branded models share visibility with partners like banks or payment processors.

You’ll also choose between consumer debit cards and business debit cards depending on your target market. Consumer cards are designed for personal spending, while business cards may include features like expense tracking, invoice management, and accounting integrations.

Think through your value proposition: what makes your card better than what users already have? Is it lower fees, better rewards, instant access to funds, or seamless integration with your platform? If you can’t answer this clearly, your adoption rates will suffer.

Step 3: Select a Bank Partner and BIN Sponsor

Your issuing bank provides regulatory coverage and access to card networks. This partnership is foundational, so choose carefully.

You will evaluate partners based on:

- Debit card experience : Have they launched similar programs before?

- Transparency on fees: Are costs clear and predictable?

- Compliance support: Will they help you navigate AML, KYC, and fraud prevention?

- Technology compatibility: Does their infrastructure integrate with your systems?

- Time to market: How long will the partnership and implementation process take?

Some banks specialize in fintech partnerships and have streamlined onboarding processes. Others may require months of negotiation and technical integration. Ask questions upfront and get clear commitments on timelines and support.

Step 4: Choose a Payment Network

Most debit cards run on Visa or Mastercard due to near-universal acceptance. Users expect to be able to use their cards at any merchant, online or in person, and these networks provide that reach.You may also need access to regional ATM networks for cash withdrawals. Without ATM partnerships, your users will face fees and limited access, which can hurt adoption and satisfaction.

Network coverage, fees, and geographic reach should match your customer base. If you're launching in the U.S., for instance, make sure your network agreements support domestic transactions and ATM access. If you’re expanding to the European Union or other regions, consider multi-currency support and international acceptance.

Step 5: Build the Technology Infrastructure

Your platform must support real-time balance checks, transaction authorization, card lifecycle management, and fraud monitoring. A mobile interface is strongly recommended for balance visibility, transaction alerts, PIN management, and digital wallet integration.

Step 6: Ensure Regulatory Compliance

In the U.S., for instance, debit cards fall under Regulation E and the Electronic Fund Transfer Act. You’ll need to tools to consider:

- Error resolution

- Transaction disputes

- KYC verification

- AML monitoring

- PCI DSS compliance

Your bank partner typically provides regulatory guidance, but accountability remains shared. You’re responsible for understanding the rules, implementing proper controls, and maintaining compliance over time. Cutting corners here can result in fines, program suspension, or legal action.

Step 7: Design Your Debit Card

Design must follow payment network branding rules and avoid restricted imagery such as explicit content, or prohibited products. Visa and Mastercard have specific guidelines on logo placement, color usage, and trademark requirements.

Physical cards must clearly display required elements like:

- Card number

- Expiration date

- Cardholder name

- Network logo (Visa, Mastercard, etc.)

- Security features (CVV, chip, contactless symbol)

Virtual card designs should also translate cleanly into digital wallets and mobile apps. Think about how your card will appear in Apple Pay, Google Pay, and other platforms. It should feel cohesive with your brand and easy to recognize.

Step 8: Launch and Distribute

Finally, you’ll decide on a phased or full launch. A phased approach lets you test with a small group first, gather feedback, and fix issues before scaling. A full launch gets your product to market faster but carries more risk if something goes wrong. Make sure support channels are live before the first cards are issued. You won’t want users contacting you with questions or problems and finding no one there to help.

Common Challenges with Debit Card Programs

Debit card programs introduce operational complexity that shouldn’t be underestimated. Fraud is especially sensitive because transactions impact user funds directly. Unlike credit cards, where the bank absorbs losses, debit card fraud hits users immediately. Real-time monitoring, instant card controls (freeze, block, replace), and strong authentication methods are critical to maintaining trust.

Customer disputes must be handled quickly. If a user reports an unauthorized transaction, you have specific legal timelines to investigate and resolve the issue. Missing those deadlines can result in regulatory penalties and user dissatisfaction.

ATM access expectations can also be challenging without the right network partnerships. If users can't withdraw cash easily or face high fees, they’ll abandon your card for alternatives that work better.

Finally, maintaining accurate real-time balances is non-negotiable. Any lag can erode trust and create overdraft risk, making infrastructure quality a top priority. Your systems need to track every transaction, update balances instantly, and prevent users from spending money they don't have. Get these fundamentals right, and your debit card program can become a powerful tool for growth. Get them wrong, and it’ll have been all for nothing.

Skip the Grind: Launch with Tap Instead

Here’s the truth: building a debit card program from scratch means months of talks, compliance setup, technology integration, and ongoing operational overhead. It's doable, yes. But it’s not quick, and it’s definitely not cheap.

Tap offers a faster path. Our white label card platform handles the heavy lifting, so you can focus on what you care about: your product and your users. While building from scratch can take a year or more, Tap enables you to launch a fully branded debit card program in as little as 12 weeks.

Tap’s platform is built for flexibility and growth. Whether you’re issuing your first hundred cards or scaling to hundreds of thousands, the infrastructure adapts to your needs. Cards are fully customizable, allowing you to create a payment experience that feels like an authentic extension of your brand.

Ready to explore what a tailored debit card program could do for your business? Get in touch with our team today.

Payments are not what they used to be. Credit cards used to be the exclusive domain of banks, but white label cards and embedded payment solutions have turned this plastic item that used to sit in your wallet into a product with personality that non-financial brands can now bring to market. Industry projections estimate the global white label card market will grow to $33.72 billion by 2032.

So, what's driving this big shift? In recent years, businesses have discovered that integrating payments and financial services directly into their customer journey isn't just convenient, but game-changing for both users and revenue.

If you want to launch a branded credit card program, we will share with you the secrets to create a credit card that aligns with your business model, generates new revenue streams, and boosts customer loyalty. A good credit card program has the potential to increase purchasing frequency, deepen brand engagement, and provide valuable transaction data.

But mind you, launching a credit card comes with its own set of challenges. And it’s not a small one. It demands significant resources, careful planning, regulatory compliance, technology, and long-term commitment. We will show you how credit card programs work, the challenges involved, and the step-by-step process required to bring one to market.

Understanding the Credit Card Ecosystem

Key Players in Card Programs

A credit card program relies on a network of participants working together. At the center is the issuing bank or credit union, i.e., a regulated financial institution that extends the line of credit and holds the cardholder accounts. Businesses launching card programs do not become banks themselves but rather partner up with an issuing bank that operates under financial regulations.

Payment networks you may be familiar with such as Mastercard, Visa, or American Express provide the global infrastructure that routes transactions between merchants, payment terminals, and banks. These networks set operating rules and acceptance standards across retail and e-commerce settings. Payment processors handle the technical execution of transactions. They authorize purchases, manage settlements, apply fraud controls, and make sure that money moves correctly between accounts.

Who Should Launch a Credit Card Program?

Credit card and debit card programs are not limited to traditional retail banks. As we discussed earlier, they are increasingly used by businesses that already manage transactions, customer accounts, or recurring payments.

Companies with strong loyalty programs, such as retail and lifestyle brands, often use credit cards to reward repeat purchasing with cashback or exclusive benefits. Marketplaces and multi-sided platforms integrate cards to streamline purchasing and settlement between buyers and sellers.

Travel and leisure businesses are another common example. By embedding a credit card into booking or expense, they reduce friction for end users and therefore capture more value per customer. Fintech startups and neobanks can also launch cards as part of a broader mobile banking or personal finance offering. Across these examples, successful programs share common traits: an existing customer base, regular transaction volume, a clear incentive for adoption, and the financial capacity to invest upfront.

Challenges You’ll Need to Overcome

Launching a credit card program involves much more than product design. Regulatory compliance is one of the most important and complex challenges you will need to tackle. You will need to comply with PCI DSS standards, KYC and anti money laundering (AML) requirements, consumer protection laws, and data privacy rules that vary by jurisdiction. These requirements are manageable but demand expertise and oversight.

Technology is another challenge. Security vulnerabilities or software bugs can quickly erode trust. For this reason, credit cards require secure, scalable infrastructure that integrates with payment networks, fraud prevention systems, apps, and customer support tools. Beyond development and compliance, your business needs to fund customer support, marketing, fraud losses, and all operational costs.

How to Launch Your Own Credit Card: Step-by-Step Process

Step 1: Define Your Strategic Goals

Before anything else, get clear on why you want to launch a credit card. The programs that succeed are the ones solving real problems for real people. That can be making purchasing easier, giving customers better expense control, or rewarding loyalty in meaningful ways. Are you chasing revenue? Trying to keep customers around longer? Trying to stand out? All of the above? Pin that down.

You will also want to get specific about your target market. What do their spending patterns look like? How do they make decisions about money? What's their credit history telling you? Set up success metrics from day one. Keep track of things like transaction volume, active cards in circulation, customer lifetime value, and how much revenue the program contributes to your business. A simple document that gets everyone on the same page is worth its weight in gold.

Step 2: Find the Right Partners

Here’s where things get interesting. You could go the full build route and create your own infrastructure, negotiating directly with banks, the whole nine yards. This gives you maximum control and the ability to customize everything, but it’s a big undertaking. We're talking months or years of work and serious resources. It is best suited to large enterprises with unique requirements and massive transaction volume.

That's why most businesses opt for a card-as-a-service model instead. These platforms handle the end-to-end infrastructure, regulatory compliance, and banking relationships so you don't have to. This approach typically allows for launch within three to six months with lower upfront investment and lower risk.

Step 3: Build or Integrate Technology Infrastructure

Your technology choices will shape both the user experience and scalability. White-label solutions offer faster deployment with limited customization, while embedded solutions allow deeper integration into your mobile app or website. You will need to take care of components such as card issuance and management systems, transaction processing, fraud and risk controls, reporting tools, and customer dashboards.

Step 4: Navigate Regulatory Requirements

Compliance is a continuous process, not a one-time task to take off your to-do list. You will deal with PCI DSS standards, KYC and KYB procedures, anti-money laundering monitoring, consumer protection regulations, and data privacy laws that vary depending on where you operate. Businesses often bring in specialized compliance counsel and rely on partners to manage much of the operational workload. Cutting corners in this area can result in fines, program suspension, or reputational damage.

Step 5: Design for User Experience

User experience plays a major role in adoption. Card design should reflect your brand while meeting payment network requirements. Onboarding should be mobile-first, crystal clear, and efficient. Nobody wants to wade through confusing terms or hidden fees. Cardholders should have real-time visibility into transactions, balances, limits, and rewards. Customer support must also be accessible and responsive.

Step 6: Test Thoroughly Before Launch

Before launch, you will need to conduct extensive testing. This includes internal testing of all transaction types, closed beta programs with a limited user group, stress testing for high transaction volume, and security assessments. Testing helps uncover technical issues, refine fraud rules, and prepare support teams. Consider at least a few extra weeks for this

Step 7: Launch Smartly

Going all-in on day one can be tempting, but a phased rollout is usually smarter. Launching first to existing customers or a specific segment allows you to monitor performance and adjust before scaling. Marketing, sales, and customer support teams should be aligned around a clear value proposition. Incentives such as introductory rewards can accelerate early adoption, but your messaging should focus on long-term value, not just short-term promotions. You want customers who stick around.

Step 8: Monitor, Optimize, and Scale

After launch, treat your credit card like the living product it is. Track metrics such as activation rate, transaction frequency, fraud levels, customer support volume, and customer lifetime value. Regular performance reviews will inform future improvements and your decision-making. Over time, you can expand features, enter new markets, and explore additional partnerships to grow the program sustainably.

Credit Card Programs for Startups

Launching a credit card program is a fundamentally different project from issuing a debit card. While both are payment cards and bring similar benefits, credit cards will introduce lending and long-term risk management into your business model. But for the right startup company, credit cards can be a game changer.

How Credit Cards Differ from Debit Cards for Startups

The most important distinction is credit risk. A credit card extends a revolving line of credit rather than spending from a bank account or deposit balance. This means your company must support underwriting, interest calculation, settlement deferral, and regulatory compliance tied to lending.

Credit cards typically generate higher interchange and fee revenue than debit cards, but they also come with higher costs. These include underwriting systems, fraud modeling, dispute handling, and compliance with laws such as the Truth in Lending Act and fair credit regulations. Time to market is usually longer too. For fintech startups, credit cards are often positioned as a premium product layered on top of an existing debit card or wallet experience.

When a Credit Card Program Makes Sense for a Startup

Credit cards are best suited for startups that:

- Have a clearly defined target market with predictable spending habits

- Want to monetize through interest, fees, and loyalty programs, not just interchange

- Are building long-term customer relationships rather than transactional usage

- Can leverage data, scoring models, and customer insights for underwriting

- Have sufficient funding to support credit exposure and regulatory overhead

Some examples can be B2B expense platforms, student or freelancer-focused financial products, retail-linked loyalty cards, and premium consumer fintech brands.

Scaling and Measuring Success

Successful credit card programs focus on:

- Card activation and usage frequency

- Customer lifetime value and repayment behavior

- Balance growth and portfolio performance

- Engagement marketing through incentives and rewards

Is Launching a Credit Card Right for Your Business?

Before moving forward, it is important to assess readiness. Businesses are typically well-positioned if they serve more than 10,000 active users, have stable revenue, and see clear demand for integrated payment or credit solutions. An upfront investment of hundreds of thousands of dollars is to be expected, along with a six to twelve month timeline before meaningful revenue is generated.